Planning for the ups and downs of the general aviation market

August 10, 2018

August 10, 2018

Understanding change is important when helping airports manage turbulence in a dynamic market

Every aircraft that passes over your head fits into one of three broad categories: commercial, military, or general aviation. Commercial includes air carrier flights (United, American, Air Canada, Jet Blue, etc.) and other commercial operations, such as air taxi charter flights. Military is self-explanatory. General aviation (GA) encompasses the remaining and broad range of flying: business travel, agricultural aviation, flight training, aerial firefighting, medical transport, aerial mapping, pipeline patrol, aerial law enforcement, sightseeing, search and rescue, personal travel, recreational flying, and much more.

Over the past five decades the GA industry has grown and retracted and made way for new aircraft types. Consider: a powered parachute soaring at treetop level on a quiet evening is GA; so too is a Gulfstream flying from New York to Los Angeles with a passenger load of business executives. Even large aircraft such as a Boeing 747 or Airbus A320, if operated for non-commercial purposes, is considered GA.

Now a major shift in the market, from recreational piston aircraft to business jet aircraft, is impacting the landscape of many US airports.

Erv Deck’s passion for flying hasn’t waned since his first solo nearly 50 years ago. Erv is pictured at Wiscasset Municipal Airport, Maine, in August 2018.

GA includes a variety of airplanes, pilots, and operations. However, the most common type of GA aircraft remains recreational piston-powered aircraft like the Cessna 172 Skyhawk.

I first soloed in a Cessna 172 Skyhawk nearly 50 years ago. The 1970s were GA’s untroubled decade, with deliveries of new airplanes peaking at about 18,000 units in 1978. By 1994, light aircraft production had fallen to just 3,000 units. This precipitous decline was the result of many factors, including the effects of product liability on aircraft manufacturers, rising fuel costs and insurance rates, inflation, and an economic recession.

That same year, Congress came to the rescue with passage of the General Aviation Revitalization Act (GARA), a statute that counteracted the effects of prolonged product liability on general aviation aircraft manufacturers by limiting the duration of their liability for the aircraft they produce. The purpose of the Act was to reverse the industry’s downward spiral. The major aircraft manufacturers, such as Cessna, Piper, and Beechcraft responded. Although production of GA aircraft, and aerospace jobs, continued to increase over time, it never returned to historic levels of the late 1970s.

Cessna 172 Skyhawk.

Today, GA still represents the most significant percentage of civil aircraft in the US, numbering more than 210,000 aircraft, from corporate jets to gliders. According to the General Aviation Manufacturing Association (GAMA), key features of the GA industry today include:

Given the scale of the GA industry, and the many variables that impact operational and financial success, our aviation planners are assisting airport owners and operators across North America as they plan for the latest market forecast and beyond.

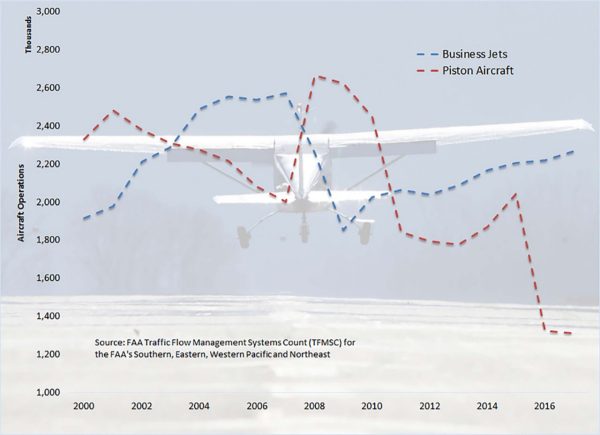

Since 2000, we’ve seen a dramatic increase in the market for business jets, while piston and turboprop aircraft demand has remained relatively flat. Not surprisingly, growth in aircraft operations mirrors the number of new aircraft. During the period from 2000–2007, business jet operations climbed sharply. After weathering a significant drop during the US recession (2008–2012), as illustrated in the above graphic, business jet activity started its long climb and has since maintained a steady growth. The Federal Aviation Administration (FAA) forecasts indicate that this trend and the downward trend for piston aircraft and operations will continue.

How does this trend in general aviation aircraft and operations impact long-term airport development?

When I began my airport planning career with Stantec in 2000, demand for airport apron (parking) space and hangar facilities was a significant issue facing many GA airports. Airports could not build hangars fast enough. Over the past several years, demand for small recreational aircraft hangars peaked at many airports. Where once operators had a long waiting list, they now have a surplus and little to no demand, resulting in falling prices for existing facilities.

Correspondingly, demand for corporate hangars and larger aircraft parking aprons has been on the rise. As the business jet market accelerates, and with the US gross domestic product showing rebound following years of stagnation, demand for the business jet market—both corporate and air taxi—will show a similar increase.

A shift in the general aviation market, from recreational piston aircraft to business jet aircraft, is impacting the landscape of many US airports.

As we partner with GA airport owners, our assessment of future demand is critical. The lead time required to plan, design, fund, and build airport infrastructure is extensive. Many airports have limited ground space within which to address the changes in size, speed, and types of aircraft.

It’s the job of an airport planner to consider the history and forecast for economics, aviation activity, and any other pertinent factors to ensure changes to an airport’s capacity and characteristics will serve the flying public in the best way possible. Planners also work closely with airport owners in maintaining a positive public image.

As many of us say in the airport business: What goes up must come down. This applies as well to the shifting business cycles in general aviation at the over 19,000 public-use airports in the US.